Insurance Applications: What Insurance Teams Ask Us Most

Insurance applications live and die by accuracy.

Across life, health, property & casualty (P&C), and specialty insurance, teams rely on complete, verified applicant data to move applications from submission to issuance without delay. Yet one detail continues to introduce outsized friction: bank account information.

That’s why we’re launching Real Questions. Real Payments. Real Answers. —a Q&A series grounded in the real conversations we have every day with insurers, managing general agents (MGAs), agencies, and technology partners, backed by what our data shows across payment activity.

This first installment focuses on insurance applications, where validating bank account details before submission or initial funding often determines whether an application moves forward—or stalls into rework.

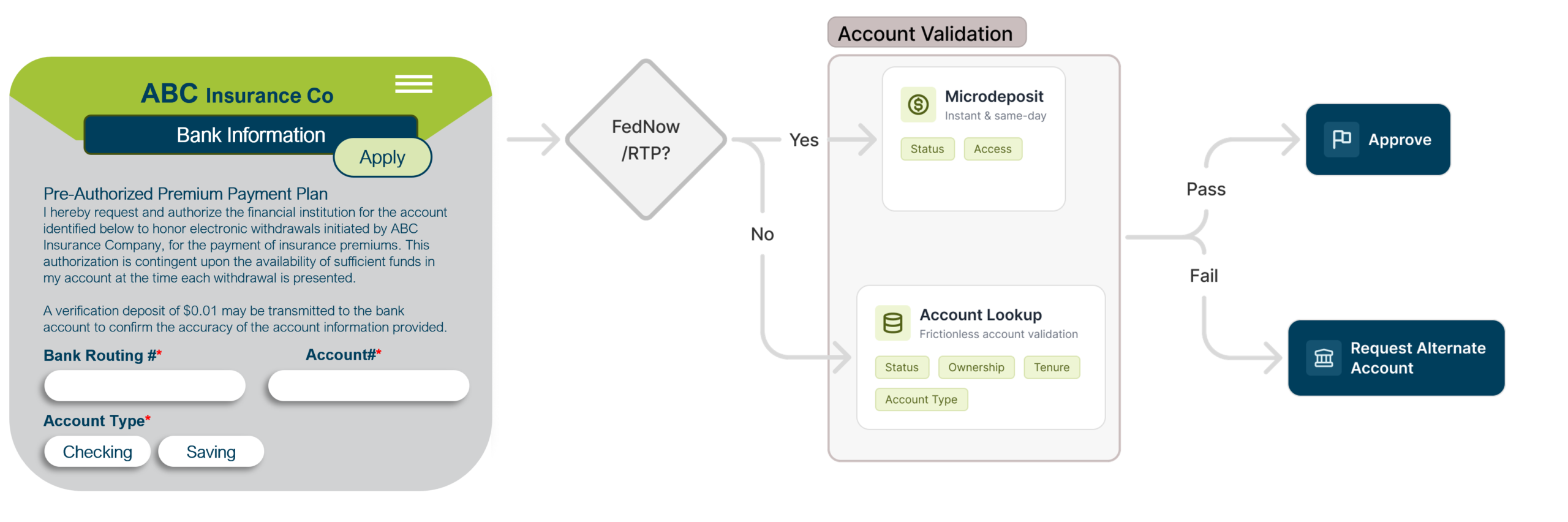

Before answering the questions insurance teams ask us most, it helps to see where bank account validation occurs during application submission and what decisions it drives at that moment.

** Sample flow. Decisioning is dynamic and configurable.

This diagram shows how validating bank account details at the point of capture connects payment eligibility, ownership, and verification signals—allowing insurance teams to approve qualified applications or intervene early, before funding issues delay underwriting or policy issuance.

Why This Matters Right Now

Over the past 24 months, U.S. insurers have expanded digital and hybrid application channels—while still relying heavily on agent‑assisted and phone‑based sales models. According to the Life Insurance Marketing and Research Association (LIMRA), nearly 70% of individual life insurance policies sold in the U.S. continue to flow through agents, reinforcing the persistence of manually supported applications across life, annuities, and specialty insurance.

At the same time, payment risk hasn’t disappeared; it’s shifted earlier. The National Automated Clearing House Association (Nacha) continues to flag elevated ACH return rates tied to administrative and account data errors, with enforceable thresholds aimed at identifying poor origination practices caused by inaccurate or manually entered bank information.

For insurers, these issues typically surface not at payout, but during application submission or initial premium funding, where incorrect or unverifiable bank details can stall underwriting, delay issuance, or trigger avoidable rework before coverage begins.

Against that backdrop, here are the questions insurance teams ask us most and what account validation reveals in practice.

❓ How can we verify a customer’s bank account before submitting an insurance application?

✅ By validating routing numbers, account numbers, and account status before the application is submitted or funded.

Incorrect or unverifiable bank information is among the most common causes of application fallout; especially in phone‑based or high‑volume sales environments. When payment details are wrong, insurers face rejected submissions, delayed underwriting, or failed initial premium collections.

Validating bank details at the point of capture shifts these issues out of underwriting and carrier funding where resolution is slower, more expensive, and more disruptive.

What the data shows*:

Across ValidiFI’s network, accounts validated as Open and Valid cleared payments at a 96.3% rate, while accounts classified as Closed or Invalid cleared at just 17.4%.

❓Can we confirm a bank account exists and belongs to the applicant without accessing balances?

✅ Yes.

ValidiFI enables insurers to confirm whether a bank account is:

-

- Real and valid for transactions

- Eligible for ACH payments

- Associated with the intended individual or business

All without permissioned login, balance access, or ongoing permissions.

This matters in regulated insurance environments where minimizing data access is as important as strengthening verification.

What the data shows*:

Validated accounts that could not authenticate ownership experienced nearly 3x higher fraudulent payment attempts than accounts with confirmed ownership.

The takeaway is simple: an account existing is not the same as the applicant controlling it.

❓Is bank account validation useful for phone‑based or non‑digital insurance sales?

✅ Yes—this is where it often has the highest impact.

In agent‑assisted and call‑center sales, applicants frequently provide payment details verbally while representatives enter them manually. Even small errors can delay coverage activation or premium collection.

Account validation helps insurers:

-

- Reduce fallout caused by data entry errors

- Avoid follow‑up triggered by failed payments

- Improve first‑time approval and funding rates

What the data shows*:

Applications supported by upfront account verification show materially lower payment setup exceptions, particularly when bank data is captured manually; leading to faster policy issuance and fewer stalled applications in high-volume environments.

❓Does account verification help with carrier portal submissions?

✅ Yes.

Carrier portals rely on accurate payment and application data. Verifying bank details before submission reduces rejections, follow‑up requests, and processing delays; especially when information is entered manually or provided directly by applicants.

What the data shows*:

In insurance-related tests where prior providers returned no usable account data, ValidiFI returned verification signals for:

- 100% of consumer accounts

- 86% of business accounts

In the same population:

- 75% of accounts passed instant verification

- Insurers were able to auto‑approve approximately 75% of payouts with fewer manual reviews

The Bottom Line

In insurance applications, bank account issues rarely look like “payment problems” at first. They surface as stalled submissions, delayed funding, and frustrated applicants.

By validating bank account details before applications are submitted or funded, insurers can:

- Improve first‑pass approval rates

- Reduce manual rework and follow‑up

- Accelerate policy issuance

- Strengthen payment accuracy without added friction

Real questions. Real answers—backed by data.

Up next: Payroll, lending, and compliance‑driven payment flows—where proactive account validation plays an even more visible role.

See how ValidiFI is powering smarter decisions before money moves. Or connect with Senior Sales Executive Ryan Chance by email or LinkedIn.

*Findings represented are based on ValidiFI internal payment risk analysis.