The biggest risk in non‑prime lending today isn’t affordability alone—it’s overconfidence in incomplete signals.

We are firmly in a consumer‑first era. Borrowers expect faster decisions and seamless experiences, while lenders must manage heightened risk, thinner margins, and increasing scrutiny around payments and fraud. Meeting both expectations requires smarter decisioning—earlier in the lifecycle.

More lenders are recognizing that traditional signals alone don’t reveal borrower intent—or the full risk story—in non‑prime lending.

Here are a few dynamics reshaping the market right now—and where lenders are finding leverage.

Affordability Pressures Demand Greater Precision

Elevated interest rates and sustained cost‑of‑living pressures continue to stretch non‑prime consumers. Payment‑to‑income ratios remain high, leaving less room for disruption or missteps.

For lenders, this means approvals must be grounded in more than surface‑level indicators. Consumer‑first strategies depend on understanding risk earlier—before loans are funded and payments are initiated.

Ability vs. Intent: Why Payment Intelligence Matters

Cashflow and income analytics answer a critical question: Can this consumer afford the payment?

But in today’s non‑prime environment, another question is just as important: How is this consumer behaving—and what risk are they not showing upfront?

Most applicants present their “best” bank account during the application process. What’s harder to see are the other accounts tied to that identity—newly opened accounts, higher‑risk institutions, or patterns that signal instability or rapid account turnover.

Understanding this broader bank account footprint adds a crucial layer of insight into intent, not just ability—an issue explored in more depth in our recent short‑term lending research: Unlocking Smarter Growth: How Consumer Lenders Can Scale Without Increasing Risk.

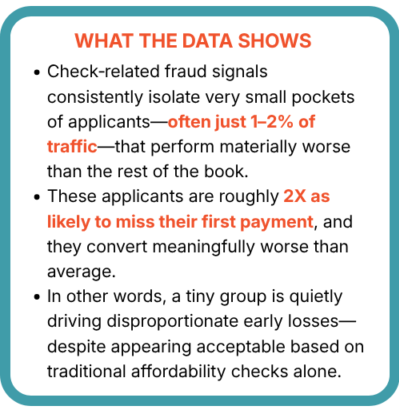

Checks illustrate this especially well. Check activity reflects how an identity has historically accessed and moved money across accounts—not just a moment‑in‑time snapshot. Repeated check usage across short‑lived or multiple accounts, links to counterfeit activity, or associations with known fraud patterns often indicate intent to extract or move funds quickly, before controls or repayment exposure materialize.

Checks illustrate this especially well. Check activity reflects how an identity has historically accessed and moved money across accounts—not just a moment‑in‑time snapshot. Repeated check usage across short‑lived or multiple accounts, links to counterfeit activity, or associations with known fraud patterns often indicate intent to extract or move funds quickly, before controls or repayment exposure materialize.

That’s why checks continue to play an outsized role in fraud risk, particularly in non‑prime lending. Even as overall check usage declines, checks still account for roughly 30% of fraud losses at U.S. financial institutions, according to Federal Reserve and AFP data. This concentration of risk makes check‑related signals one of the most efficient places for lenders to introduce early, low‑friction controls—at the very top of the decision waterfall.

Bringing Intent Insight Earlier: Account and Check‑Related Risk Signals

By analyzing identity‑level patterns across prior banking and payment activity, lenders can see beyond the single account submitted on an application.

Early account signals help confirm whether routing details are valid and active, while also surfacing patterns that may point to elevated risk. When paired with historical check‑related risk indicators, lenders gain visibility into identities associated with counterfeit activity, suspicious behavior, or known fraud patterns.

Together, these insights help lenders:

- Detect consumers cycling through high‑risk or fintech bank accounts

- Uncover risk that isn’t visible through permissioned data alone

- Reduce exposure before funding or disbursement

- Route higher‑risk applicants to additional verification earlier in the process

Many lenders are applying these signals at the very top of the decision waterfall—where low-cost checks can prevent unnecessary risk escalation, reduce downstream costs, and protect performance before funds move.

Powering Smarter Decisions in a Consumer‑First Market

Advanced data and analytics are no longer about speed alone. The real advantage comes from insight—seeing the full picture of a consumer’s payment behavior and risk posture.

When lenders can separate borrowers who can’t pay from those who won’t, they protect portfolios while delivering fairer, more responsible outcomes for consumers.

Continuing the Conversation

If you’ll be at OLA Tribal Lending Conference in May, my team and I will be there. Meet with Matt Harding, Alice Shin, and me to discuss how smarter payment and fraud intelligence is helping non‑prime lenders manage risk earlier—without adding friction to the consumer experience.

Final Thoughts

Non‑prime lending isn’t slowing down—it’s getting more sophisticated. Lenders that invest in earlier validation, deeper payment insight, and smarter fraud controls will be best positioned to compete.

At ValidiFI, we help organizations turn complex risk and payment data into confident action.

Powering Smarter Decisions.

Want to see how it works? ValidiFI It. Contact us or visit ValidiFI.com to learn more.

— Adam DiVeroli, VP, Head of Alternative Finance—ValidiFI

Adam DiVeroli is Vice President, Head of Alternative Finance at ValidiFI, where he works with non-prime and specialty lenders to strengthen decisioning across underwriting, payments, and fraud prevention. He brings deep experience helping lenders balance growth, risk and consumer-first outcomes using alternative data and payment intelligence.

![[OLA Member]](https://validifi.com/wp-content/uploads/2024/06/seal.png)